We surveyed 45 participants and conducted 8 interviews to get a better perspective on the problem.

Our objectives:

Understand how users feel regarding their financial decisions

Discover user pain points regarding facing their finances and making decisions

Pinpoint user desires and concepts/ideas that have helped them personally

Our survey participants were asked to write a short answer about the personal challenges they face with improving their financial knowledge. The majority expressed general confusion with the complexity of the concepts regarding finances.

"It feels inaccessible."

"I have limited knowledge."

"The jargon goes over my head."

"I need someone to explain things to me."

"The language is so complicated."

We noticed a pattern of avoidance coping in our interviewees responses.

Our interviewees expressed that they were chasing after the cost of living.

They only spend money on what they need and let go of the things they want.

"I’m very intimidated by investing. Time is everything, and I’m wasting it."

"I overthink things a little too much. And sometimes, I just kind of stop myself from making a decision."

"I'm just not where I want to be. I would say I'm just trying to get to the point of stability."

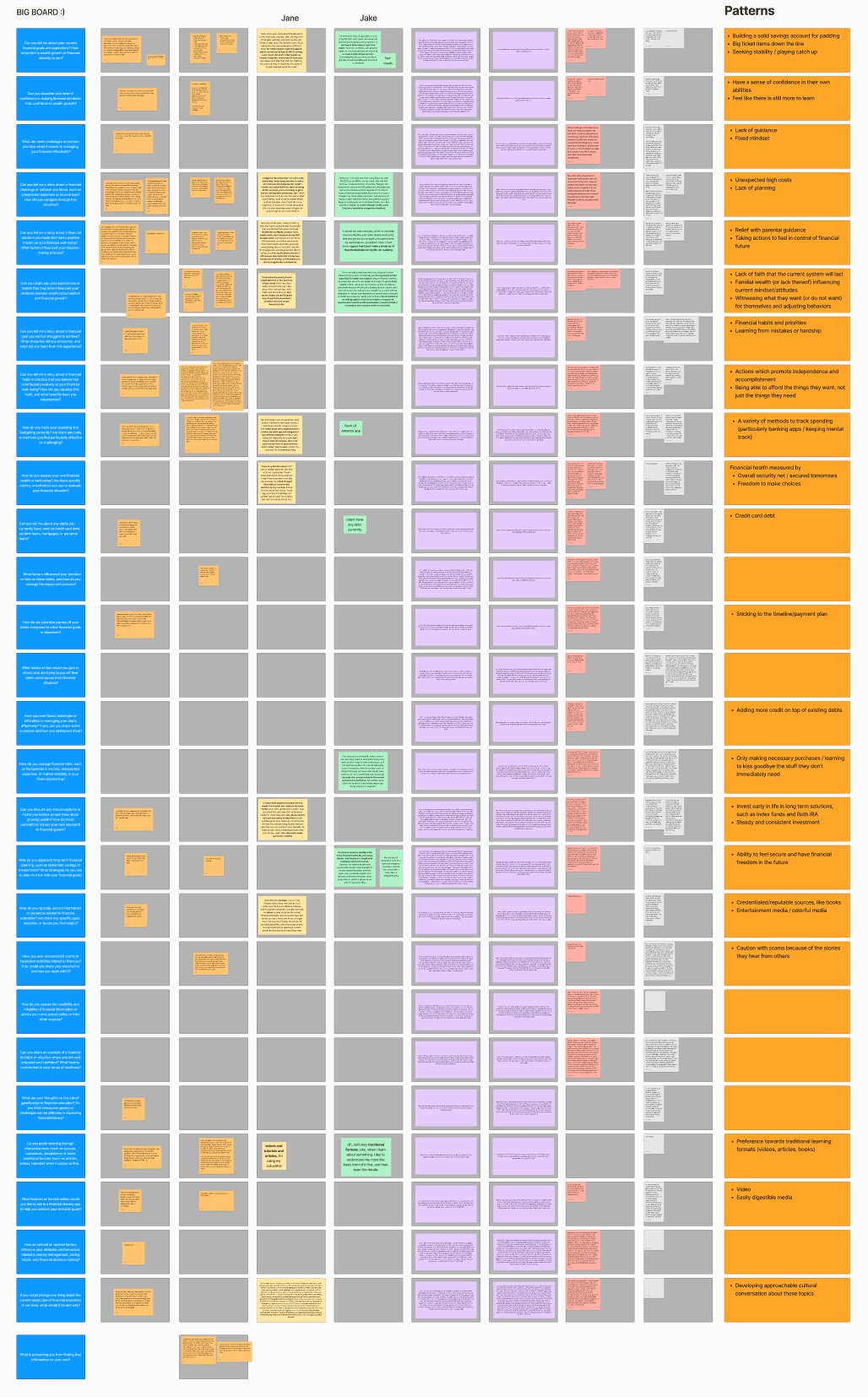

Our team utilized a big board to assess patterns in our interviewees responses to our research questions.

Our team learned that…

Finance feels unapproachable and intimidating

Most users feel that they are falling behind

They want to make the best decision about where to put their money

They worry about unexpected expenses that will break the bank

User Insights

Users need a sense of control over their money when investing in long term assets because they fear the loss of immediate liquidity due to uncertainty about tomorrow's financial stability.

Users need risk management tools because individualistic cultures encourage entrepreneurship and risk-taking, which can be beneficial for economic growth.

Users could benefit from unbiased and realistic financial benchmarks because exposure to false depictions of success on social media can create a sense of urgency to achieve similar levels of affluence, often leading users to prioritize immediate wealth and short term gains.

We observed that many users struggle with navigating complex financial concepts, indicating a widespread need for an accessible and practical resource to improve financial literacy.

Following our initial user research our team began drafting a problem statement to address the core issue our interviewees were facing.

Problem Statement

Many people struggle with managing their finances due to a lack of easy-to-access resources and personalized guidance.

This leads to poor financial decisions, debt, and limited savings.

There is a need for a user-friendly financial literacy app that provides educational content, tools, and support to help users improve their financial knowledge and achieve their financial goals.

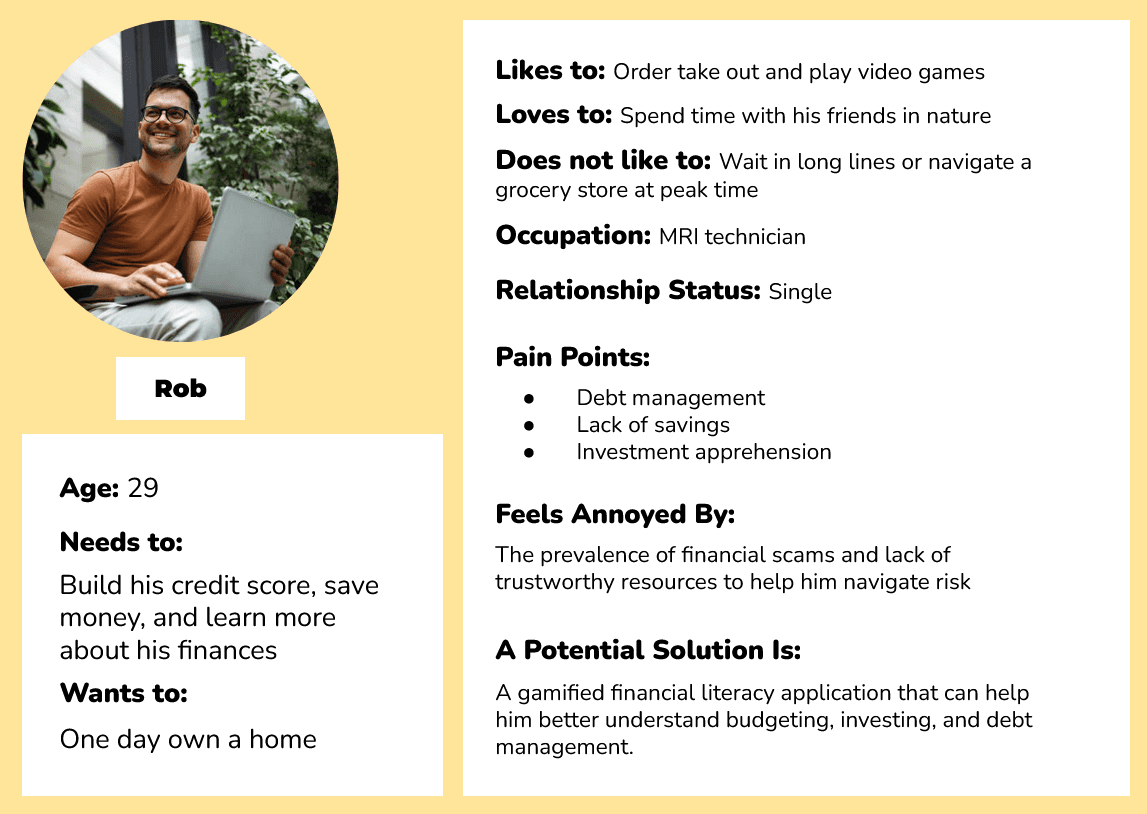

We began our research plan with theories and assumptions. We needed to narrow down who our target users would be and why.

We then developed a fictional user, Rob, to represent potential users and help us identify their behaviors, goals, wants, & needs in our screener survey.

Our team then drafted a competitive analysis to find the opportunities in the space that may have been untapped.

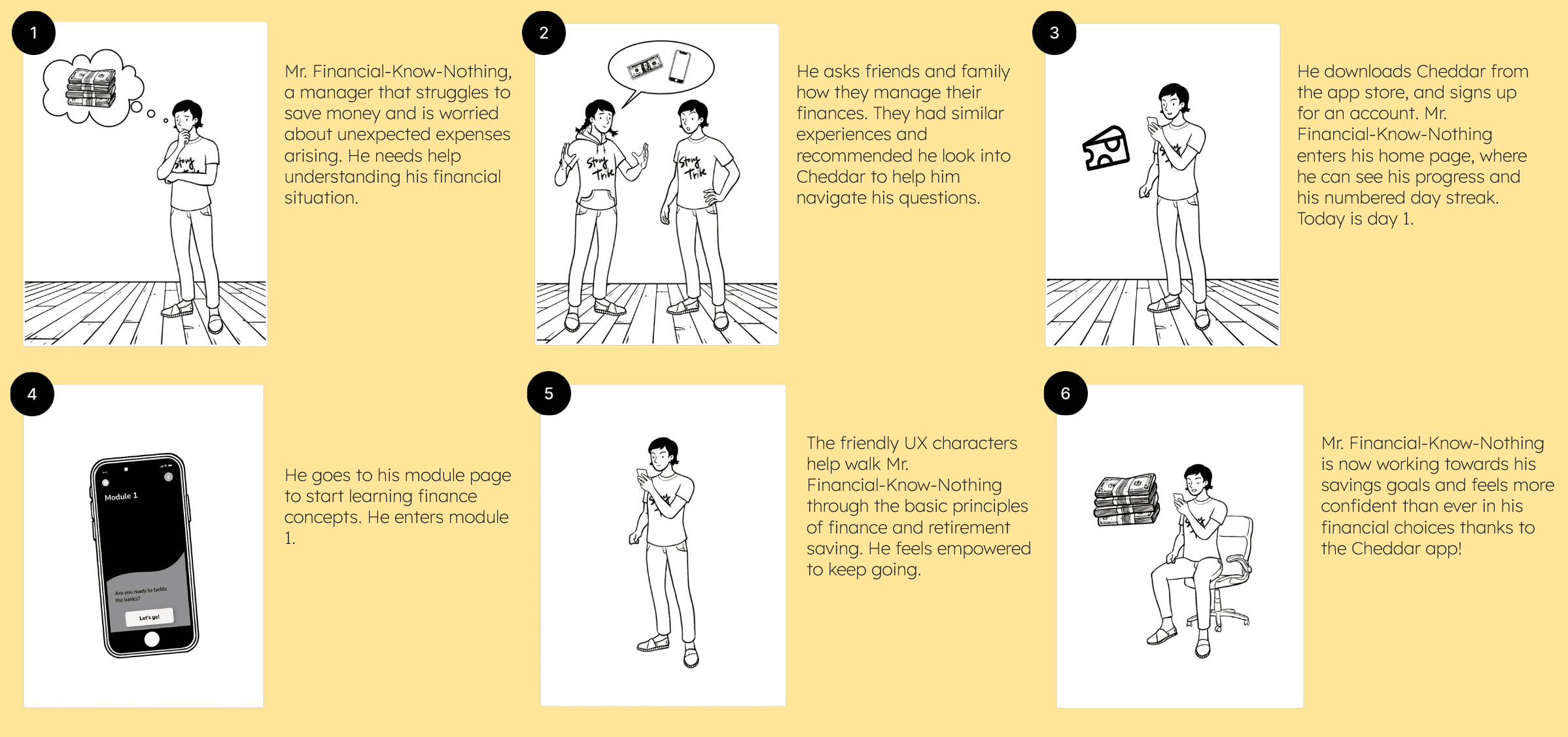

Following our competitive analysis we created a storyboard as well as a customer journey map following a proto persona, Mr. Financial-Know-Nothing through his potential interaction with Cheddar, our idea for an app targeting financial literacy to get a better idea of how our app might help him and users like him.

Our team then used the "I like, I wish, what if?" exercise to help us narrow down important needs that we wanted to meet for our users eventually taking our ideas and plotting them on a feature prioritization matrix to find what would be most feasible and helpful.

As we moved into the design phase, we created user flows and initial sketches for the app prototype using the main ideas we had picked from our feature prioritization as a template for what we envisioned would most help users.

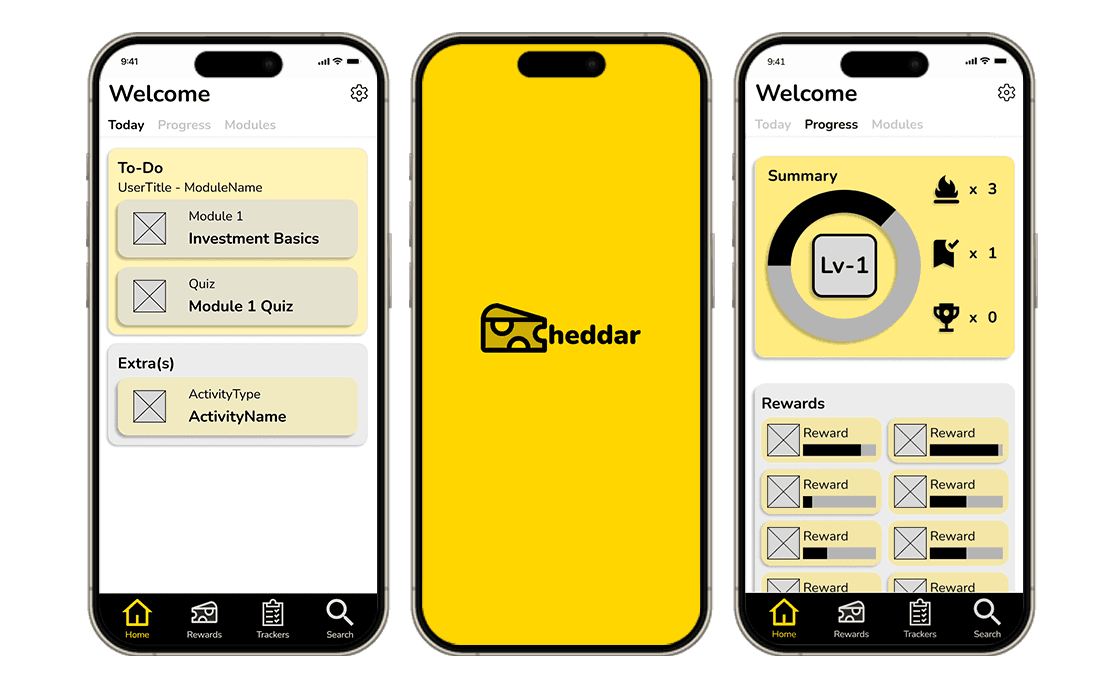

Following this we transformed out sketches into wireframes in figma and began creating an early lo-fi prototype of our solution.

Our users were tasked with testing our mid-fidelity prototype. They were assigned five specific tasks:

Navigate to module 1 from the home page

Find module 1 in recent searches

Add a debt in tracker

Add a new savings goal

Check progress on the app

Testing Results:

Missing connections on Navigation Bar

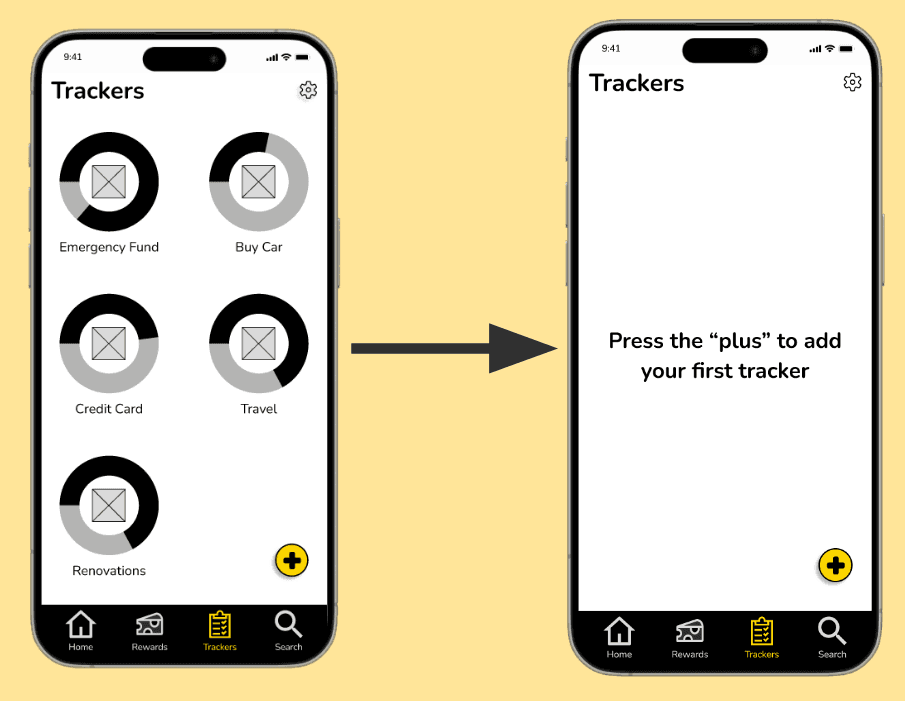

Trackers page confusing leading to point-&-guess clicking

Interactions not working

Button for adjusting time frame breaks after first press

Scroll features not working

Following the feedback we received from our user testing, we added an instruction message to the trackers page for better clarity, fixed several connections between pages for better flow through the app, and fixed several non functioning interactions.

Reflecting on our process, we discovered that our initial IoT concepts, such as smart home utility controls and personal weather stations, did not effectively address the core issues faced by users during storms, leading us to pivot towards emergency response and offline solutions.

Throughout development, we also faced scope creep as we added features to better meet user needs.

In the end, our team was proud of what we had accomplished in such a short amount of time, especially given the multiple pivots we made during development that could have potentially hurt out momentum had we not continued pushing.